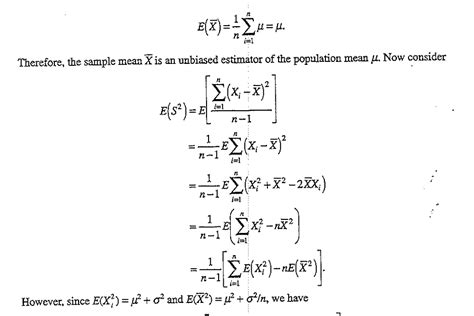

Welcome to a focused look at the Indicator Variable Squared Expectation and its role for time series analysts. This article explains Indicator Variable Squared Expectation, how it behaves for binary indicators, why it equals the probability of the event, and how to leverage this insight in forecasting, feature construction, and risk assessment.

Indicator Variable Squared Expectation: Core Idea

When I_t takes values 0 or 1, squaring yields I_t^2 = I_t. Therefore, E[I_t^2] equals E[I_t], which is the probability p_t that the event occurs in period t. This identity is foundational for time series analysts who model binary indicators, regime switches, or event-driven signals. Understanding this relation helps connect second-moment views to simple probability estimates.

In practice, this means the squared expectation of a binary indicator is often just the probability you observe in your data, which streamlines interpretation and computation in many common models.

Key Points

- For a 0/1 indicator I_t, I_t^2 = I_t, so E[I_t^2] = E[I_t] = p_t, the period probability of the event.

- Indicator Variable Squared Expectation links second moments to simple probabilities, easing interpretation in binary-event models.

- When aggregating over time, E[I_t^2] reflects the average event probability across periods, aiding comparative analysis.

- In forecasting, using E[I_t^2] can simplify risk metrics that rely on second moments of binary signals.

- Estimation typically uses observed event counts to estimate p_t, making E[I_t^2] directly estimable from data.

Applications in Time Series Analysis

The identity E[I_t^2] = p_t has several practical implications. It helps calibrate probabilistic forecasts for binary events such as regime changes, failures, or customer actions. When you build models that predict the occurrence of an event, interpreting the squared expectation as the event probability can simplify loss functions and evaluation metrics that depend on a second moment.

By anchoring second-moment thinking to a probability, Indicator Variable Squared Expectation enhances interpretability and decision-making in risk management and forecasting. This clarity can improve model communication with stakeholders who rely on probabilistic rather than abstract moment-based reasoning.

Estimation tips and practical notes

Estimate p_t from historical data as the fraction of periods where the event occurred. If you work with covariates, you can model p_t as a function of features using logistic or probit models, then use E[I_t^2] = p_t in downstream calculations. In a time series context, p_t can evolve over time, so you may employ rolling estimates or state-space approaches to track changes in the event probability.

Be mindful that real-world indicators may deviate from ideal 0/1 behavior due to measurement error or reporting lag. In such cases, E[I_t^2] still equals E[I_t] if the observed I_t remains binary, but if the data are noisy, consider modeling the latent indicator and then derive its squared expectation from the latent probability.

Limitations and caveats

While the equality E[I_t^2] = E[I_t] is exact for a clean binary indicator, many practical settings involve imperfect data, non-binary signals, or dependent indicators. In those cases, the squared expectation still provides a useful anchor, but you should check assumptions about independence, stationarity, and temporal correlation before applying it in risk metrics or hypothesis tests.

What is the Indicator Variable Squared Expectation and when should I use it?

+The Indicator Variable Squared Expectation refers to E[I_t^2] for a binary indicator I_t. For 0/1 indicators, I_t^2 = I_t, so E[I_t^2] equals the event probability p_t. Use it to connect second-moment thinking to probabilities in binary-event forecasting, risk assessment, and feature construction.

How does E[I_t^2] relate to p_t in a time-varying context?

+In a time-varying context, E[I_t^2] = p_t, so the squared expectation tracks how the event probability evolves over time, enabling dynamic forecasting and adaptive risk measures.

Can I use Indicator Variable Squared Expectation with non-binary indicators?

+The specific identity E[I_t^2] = E[I_t] holds for binary indicators. For non-binary or continuous signals, squared expectation relates to second moments but does not simplify to a probability.

What are common pitfalls when applying this concept?

+Pitfalls include ignoring data quality issues, assuming independence when there is autocorrelation, and misinterpreting second-moment calculations as probabilities for binary events without checking the underlying data-generating process.